📈 Week 30 (22-28 July 2024) Market Summary

US Stocks (Major Indices), Sector and Asset Class rotation, The Magnificent Seven, Global Stock Indices, Volatility, Major Economics Announcements and Earnings Reports

Hello! 👋

Let's take a look at what we've been up to this week.

1. US Stocks (Major Indices)

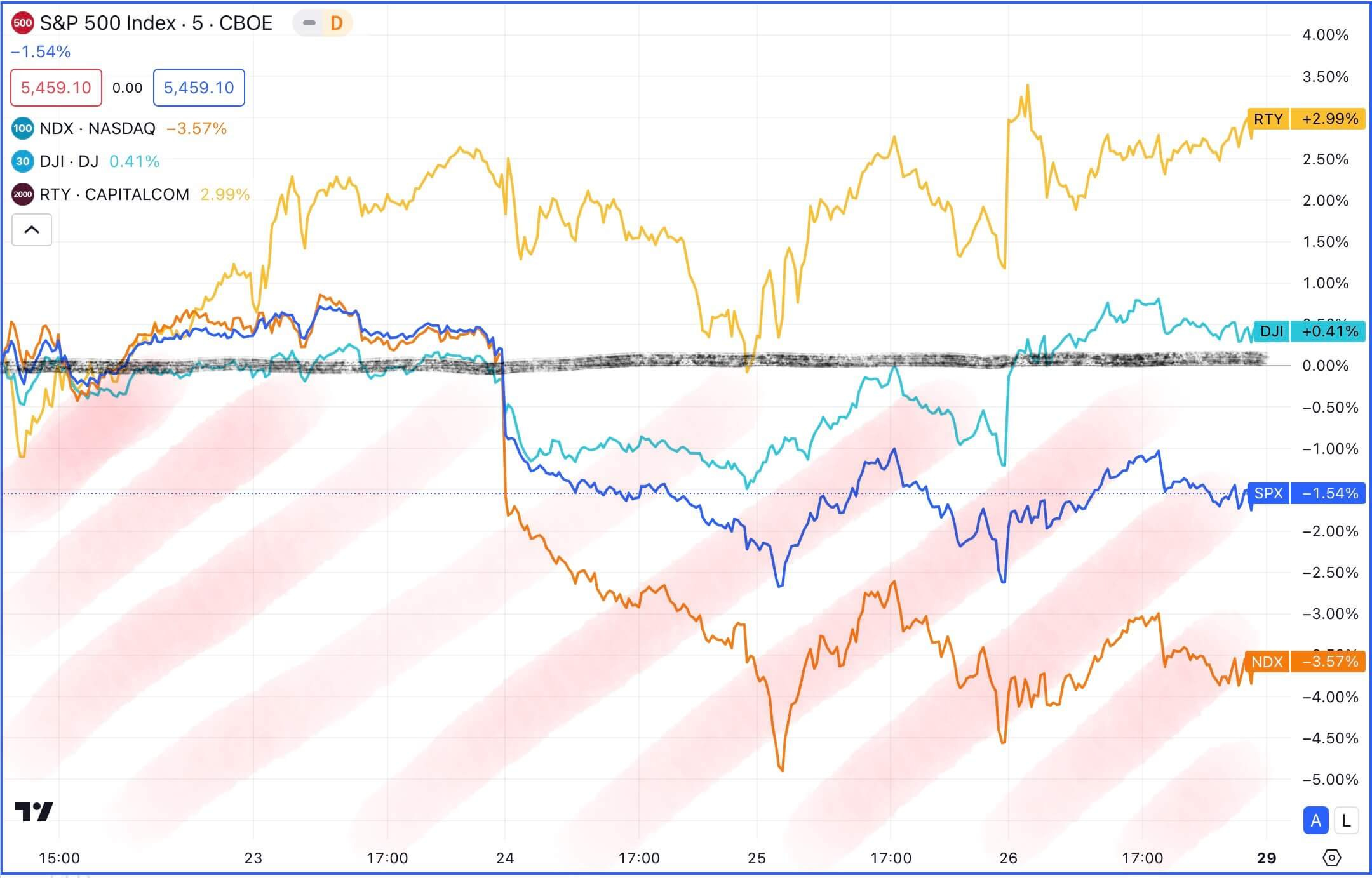

US stocks ended the week in the red. We observed that tech stocks were on sale, with capital rotating into other sectors such as Healthcare and Industrials.

The Nasdaq 100 lost the most (-3.57%) among the major US stock indices. The S&P 500 decreased by 1.54%, the Dow Jones Industrial Average remained almost unchanged, and the Russell 2000 even increased by 2.99%.

However, the Nasdaq 100 is still performing well in 2024, having increased by 14.99% this year. The S&P 500 has risen by 15.10%, the Russell 2000 has added 12.33%, and the Dow Jones (DJIA) has grown by 7.62% so far this year.

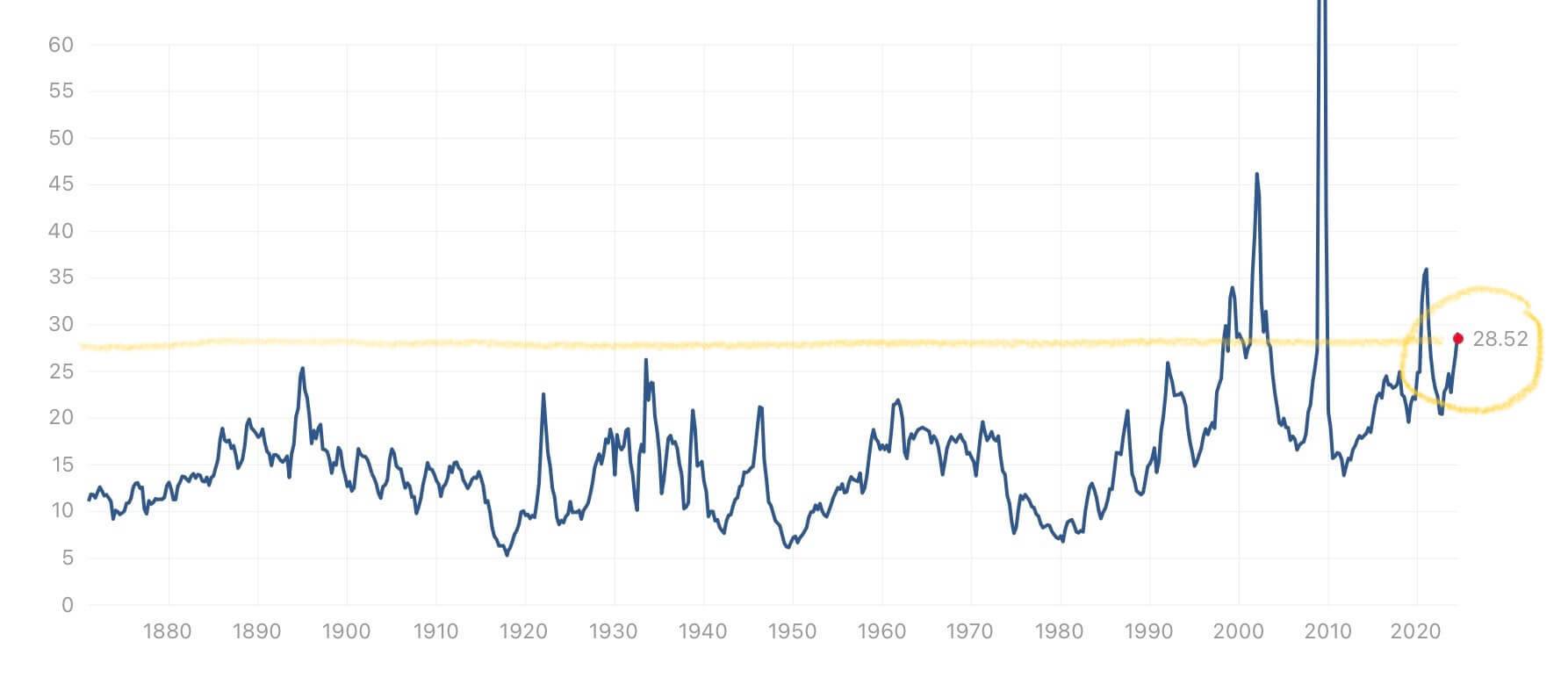

The Price/Earnings Ratio of S&P 500 index companies is currently at 28.52, which is high but not extreme.

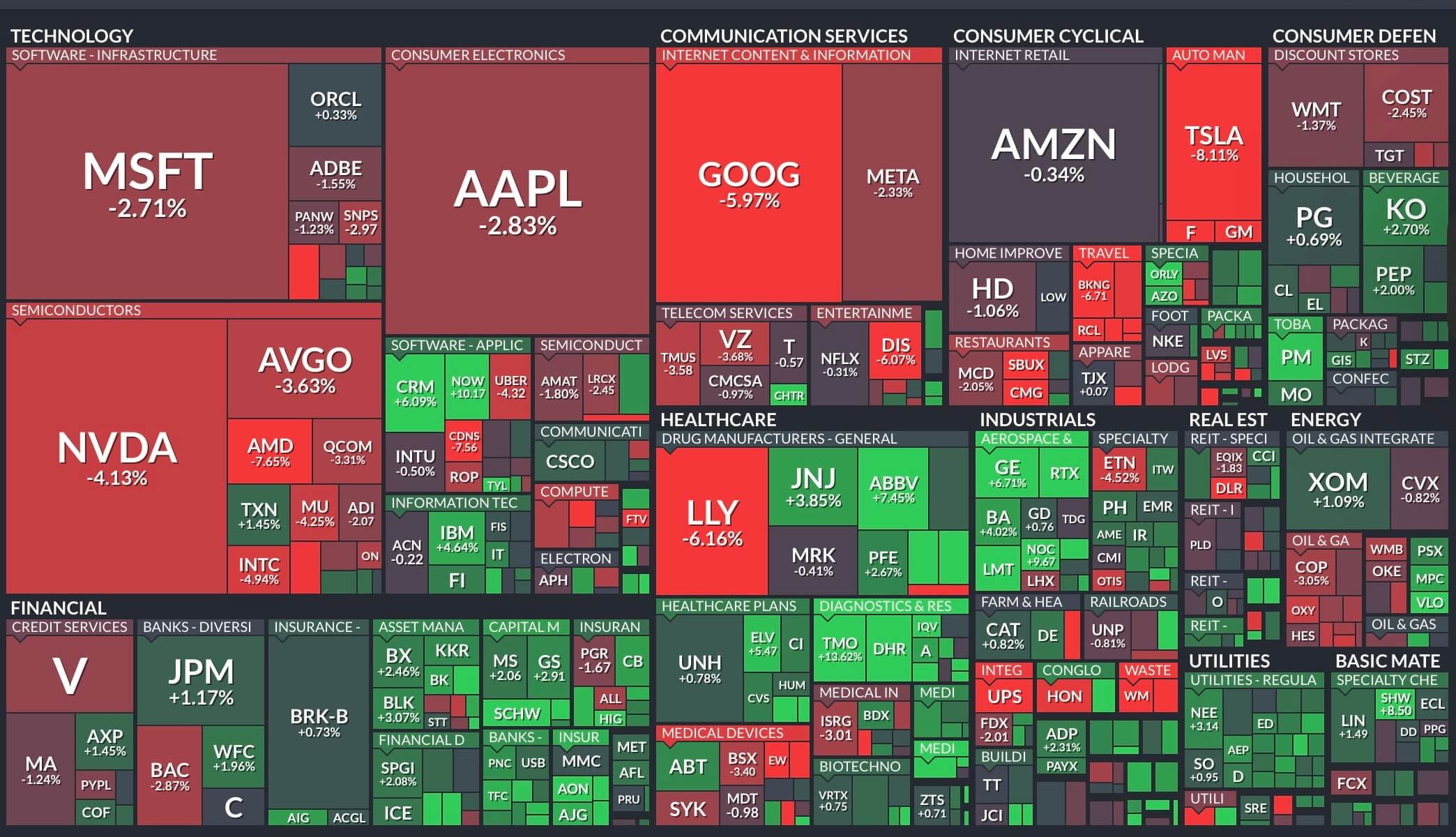

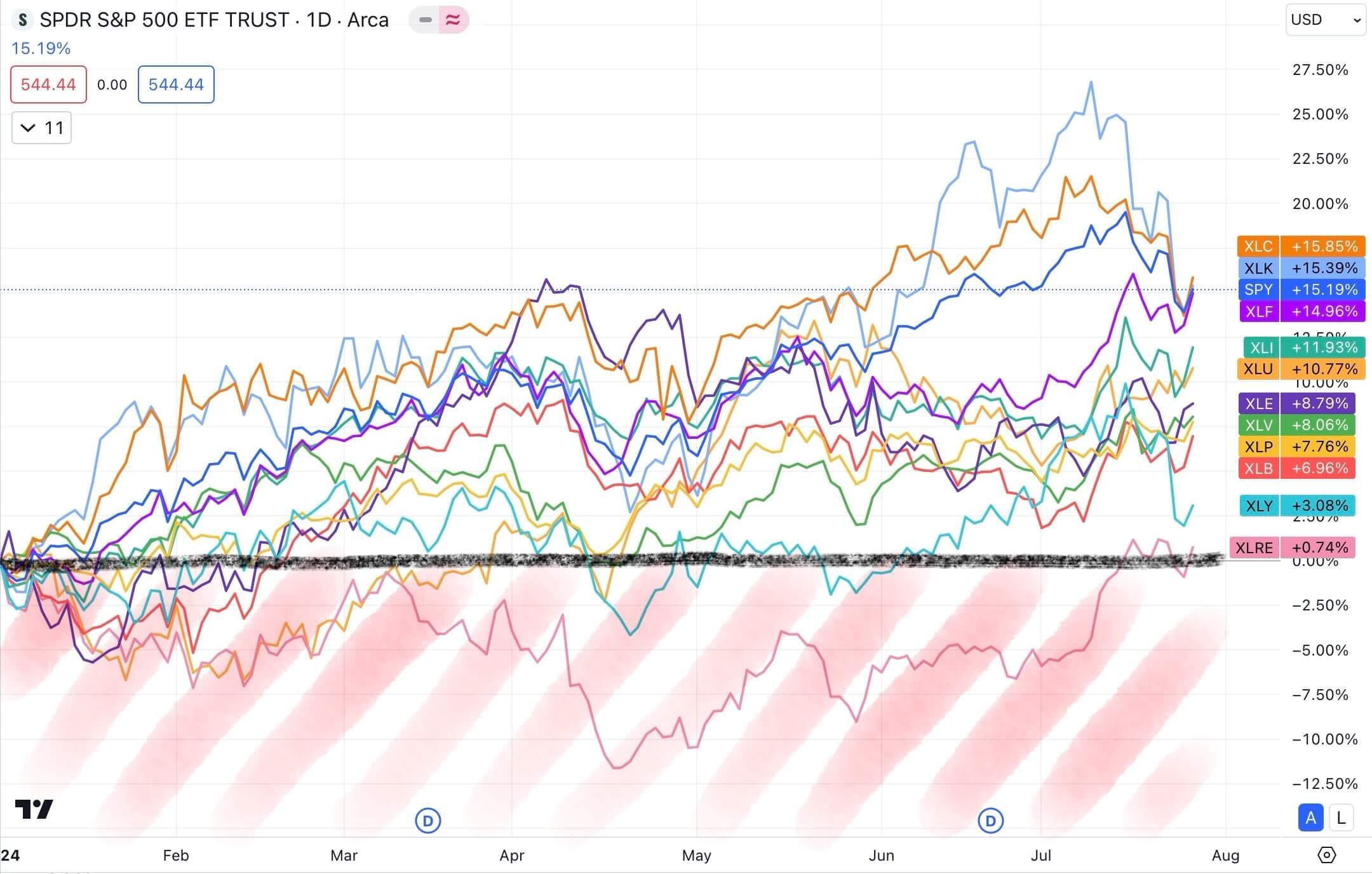

2. US Stocks by Sector

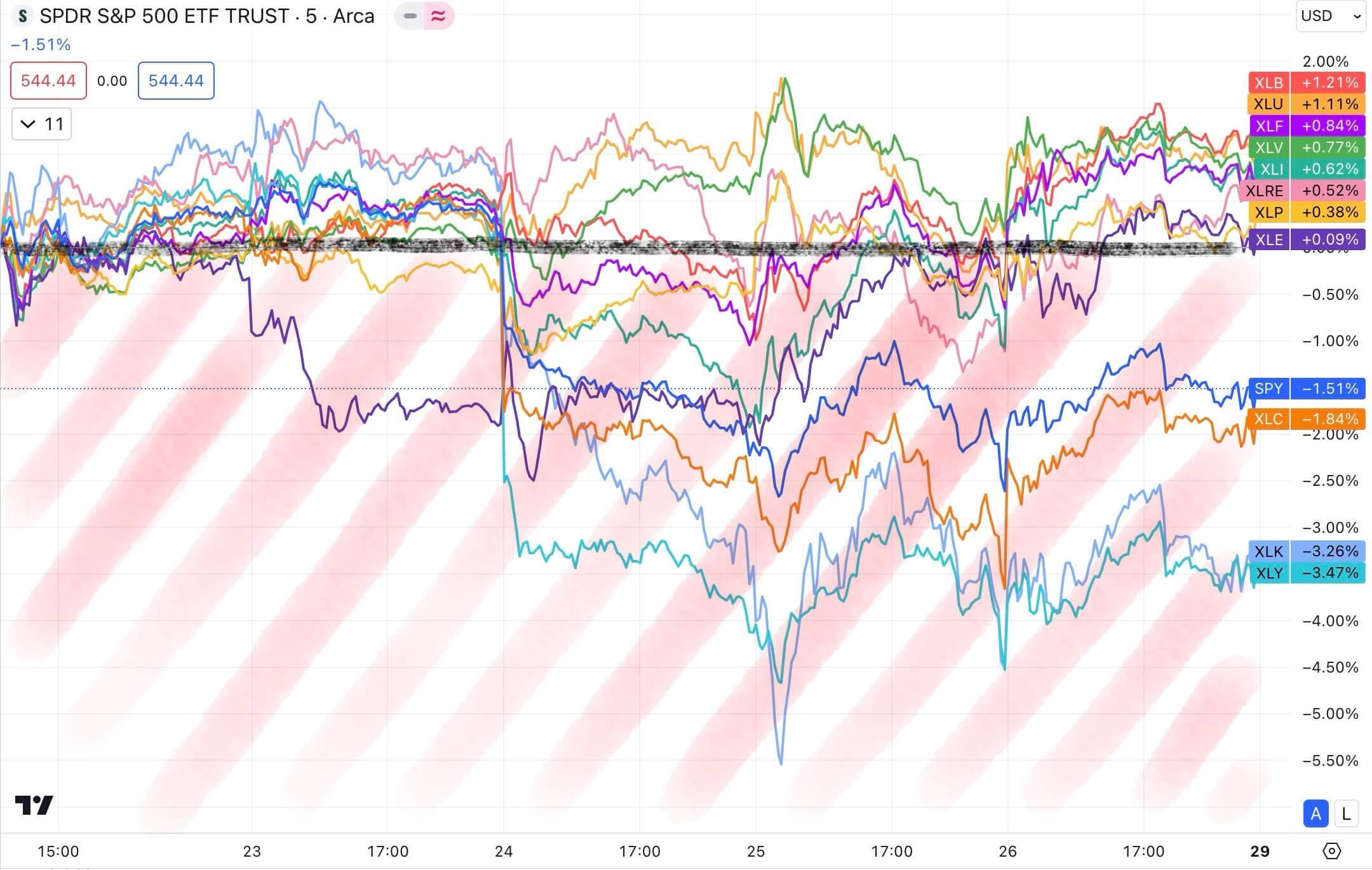

The Consumer Discretionary sector lost the most this week, followed by the Technology and Communication Services sectors. The Materials and Utilities sectors gained the most this week.

XLC - Communication Services,

XLK - Technology,

XLP - Consumer Staples,

XLE - Energy,

XLY - Consumer Discretionary,

XLF - Financials,

XLI - Industrials,

XLB - Materials,

XLV - Health Care,

XLU - Utilities,

XLRE - Real Estate,

SPY - S&P 500.

This week, the Communication Services sector became the leader in 2024 with a 15.85% gain. The Technology and Financial sectors are second and third, respectively. The Real Estate sector performed the worst this year, gaining only 0.74%.

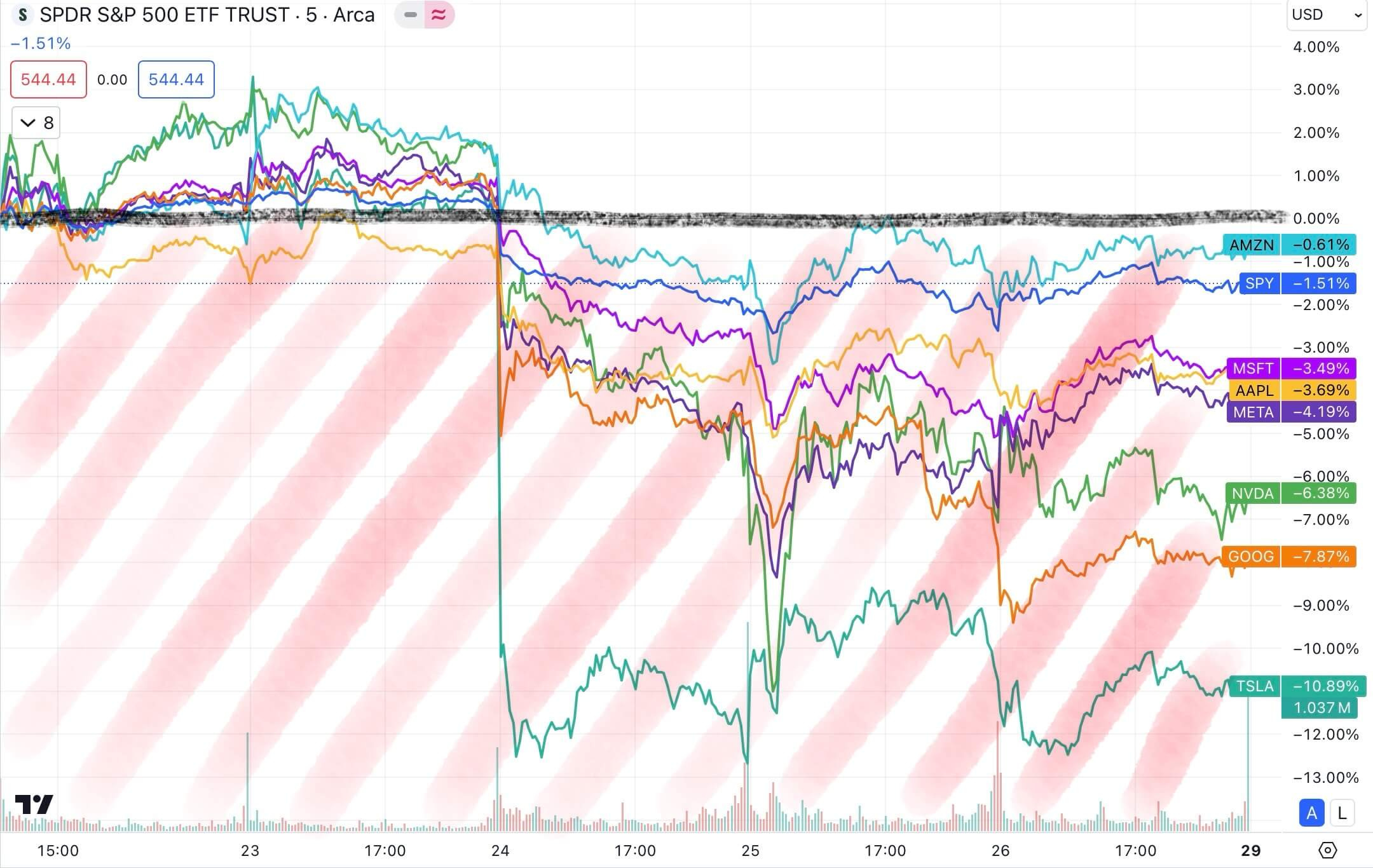

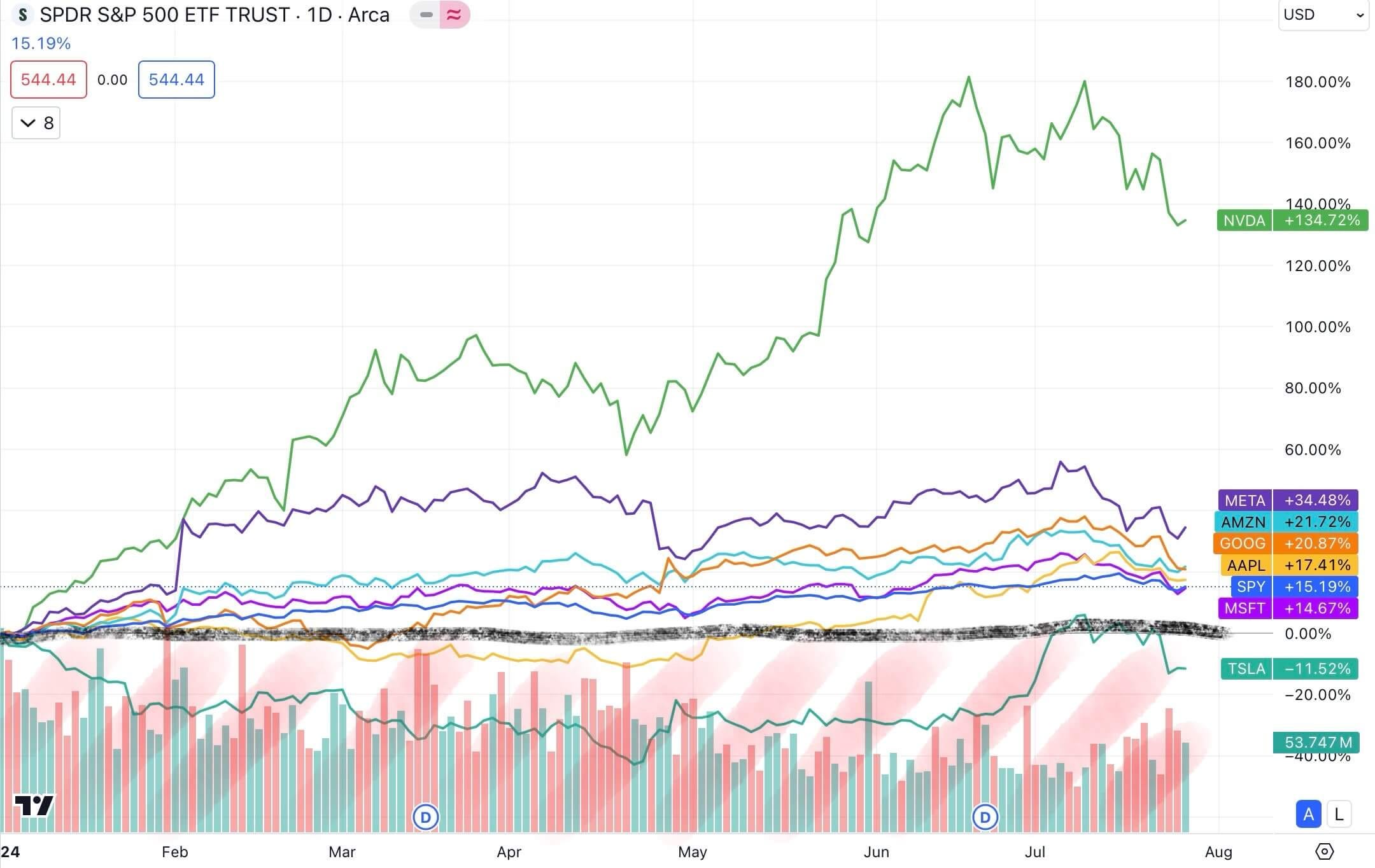

3. The “Magnificent Seven”

The Magnificent Seven stocks were all down this week, with Tesla (TSLA) losing the most (-10.89%).

However, they are all up this year except for Tesla (TSLA), with Nvidia (NVDA) being the clear leader with a 134.72% gain in 2024 so far..

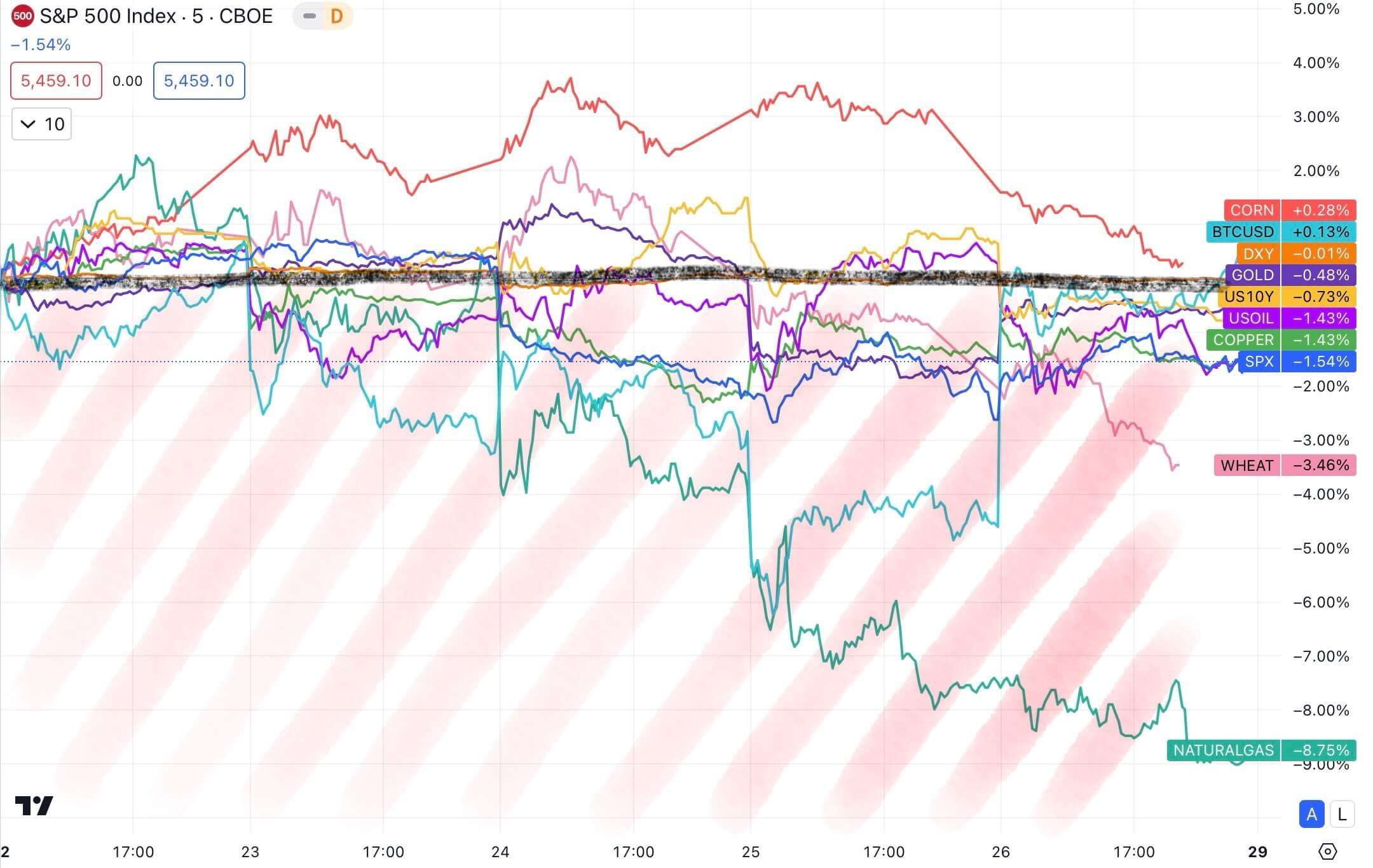

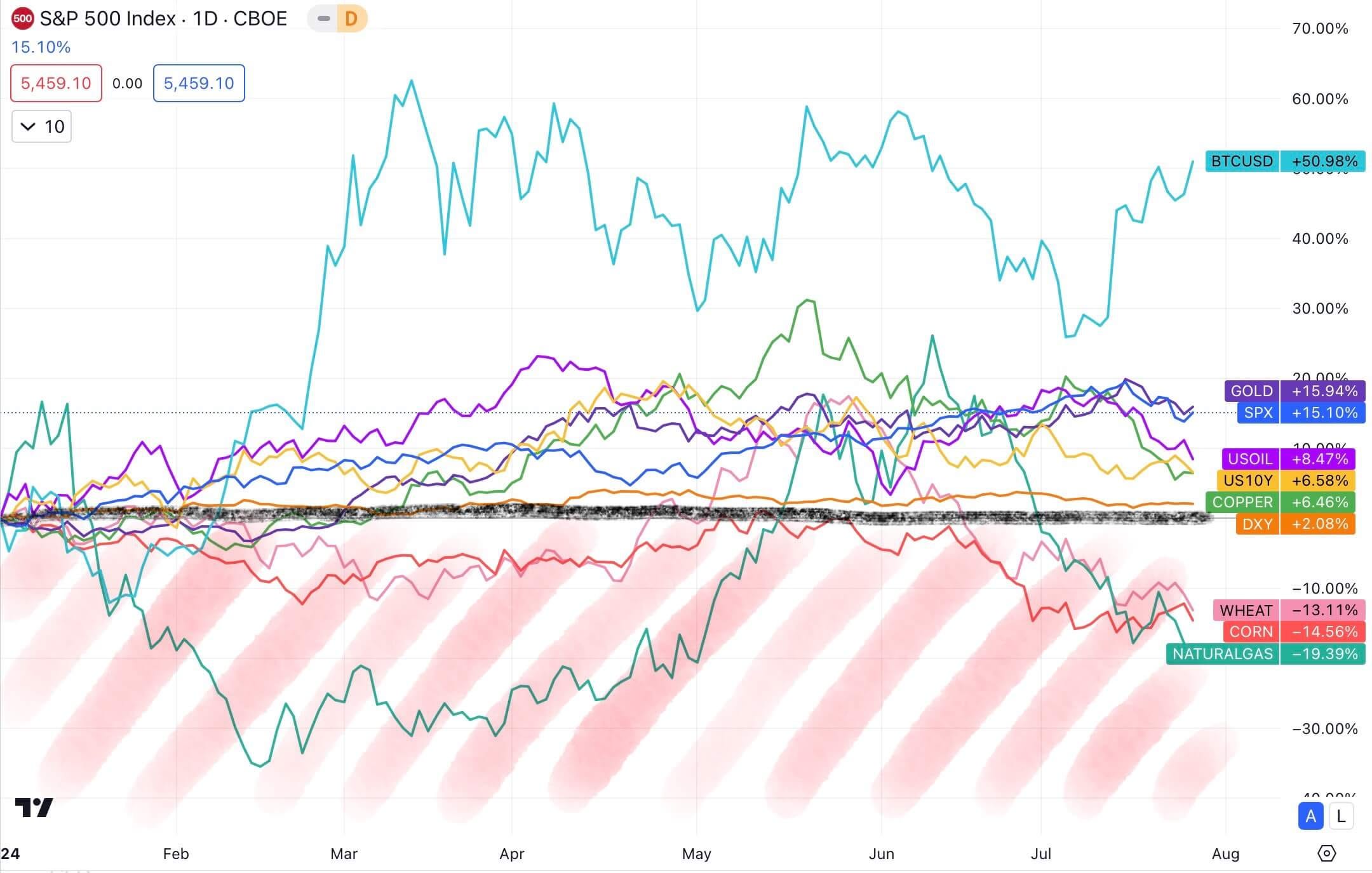

4. Asset Class Rotation (Stocks, Currencies, Commodities, Bonds)

Natural Gas and Wheat decreased the most this week, while other asset classes remained almost unchanged.

Wheat, Corn, and Natural Gas are down this year, while stocks, metals, and Bitcoin are up.

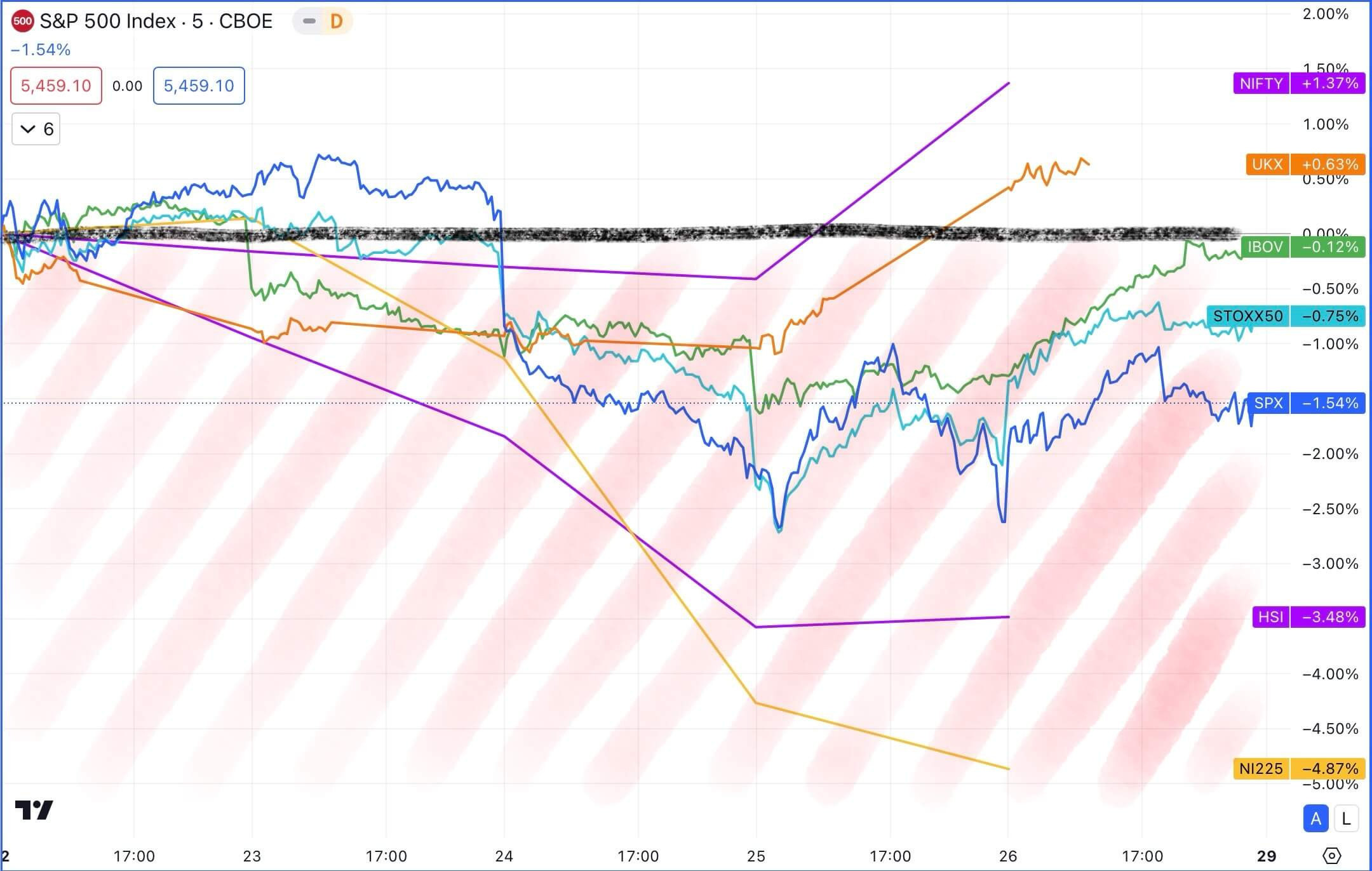

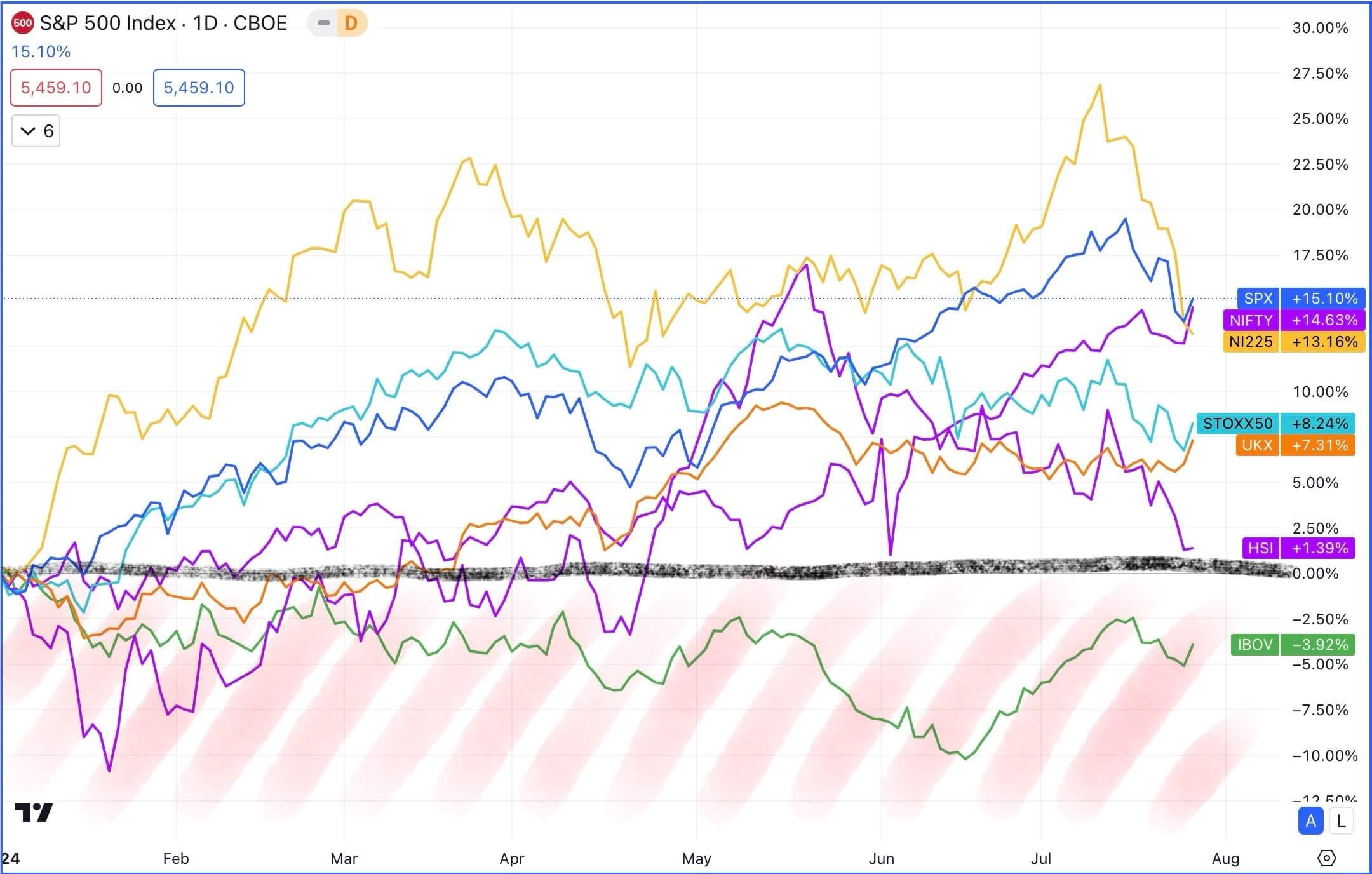

5. Global Stock Markets

Global stocks were also down this week, with Japan and China losing the most. India and the UK gained slightly.

USA (SPX) - S&P500 Index,

UK (UKX) - FTSE100 Index,

Europe (STOXX50) - EURO STOXX 50 Index,

Japan (NI225) - Nikkei225 Index,

China (HSI) - Hang Seng Index,

India (NIFTY) - Nifty50 Index,

Brazil (IBOV) - BOVESPA Index.

Japan, India, and the US have gained the most in 2024 so far, while the Brazilian BOVESPA has lost 3.92% this year.

6. Volatility

The VIX futures term structure indicates that there is hedging activity going on around the US Presidential Election.

The VIX index closed above 16 this week, indicating that fear has returned to the market.

The Volatility of Volatility Index (VVIX) indicates an increase in demand for VIX index products, meaning that market participants were willing to pay more for hedging products.

“The SKEW index measures tail risk—returns two or more standard deviations from the mean—in S&P 500 returns over the next 30 days. The primary difference between the VIX and the SKEW is that the VIX is based on implied volatility around the at-the-money (ATM) strike price, while the SKEW considers implied volatility of out-of-the-money (OTM) strikes.” (more at Investopedia.com)

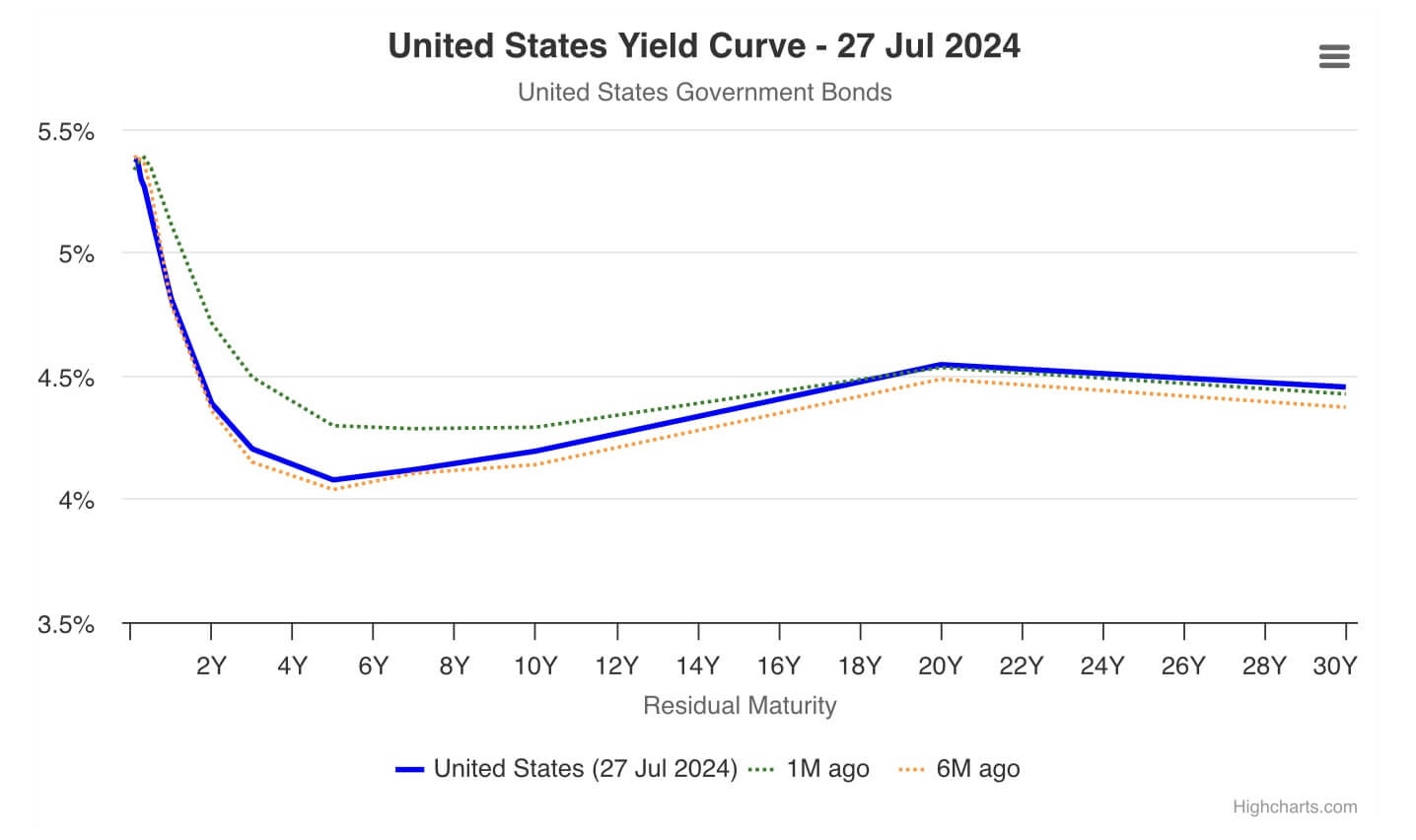

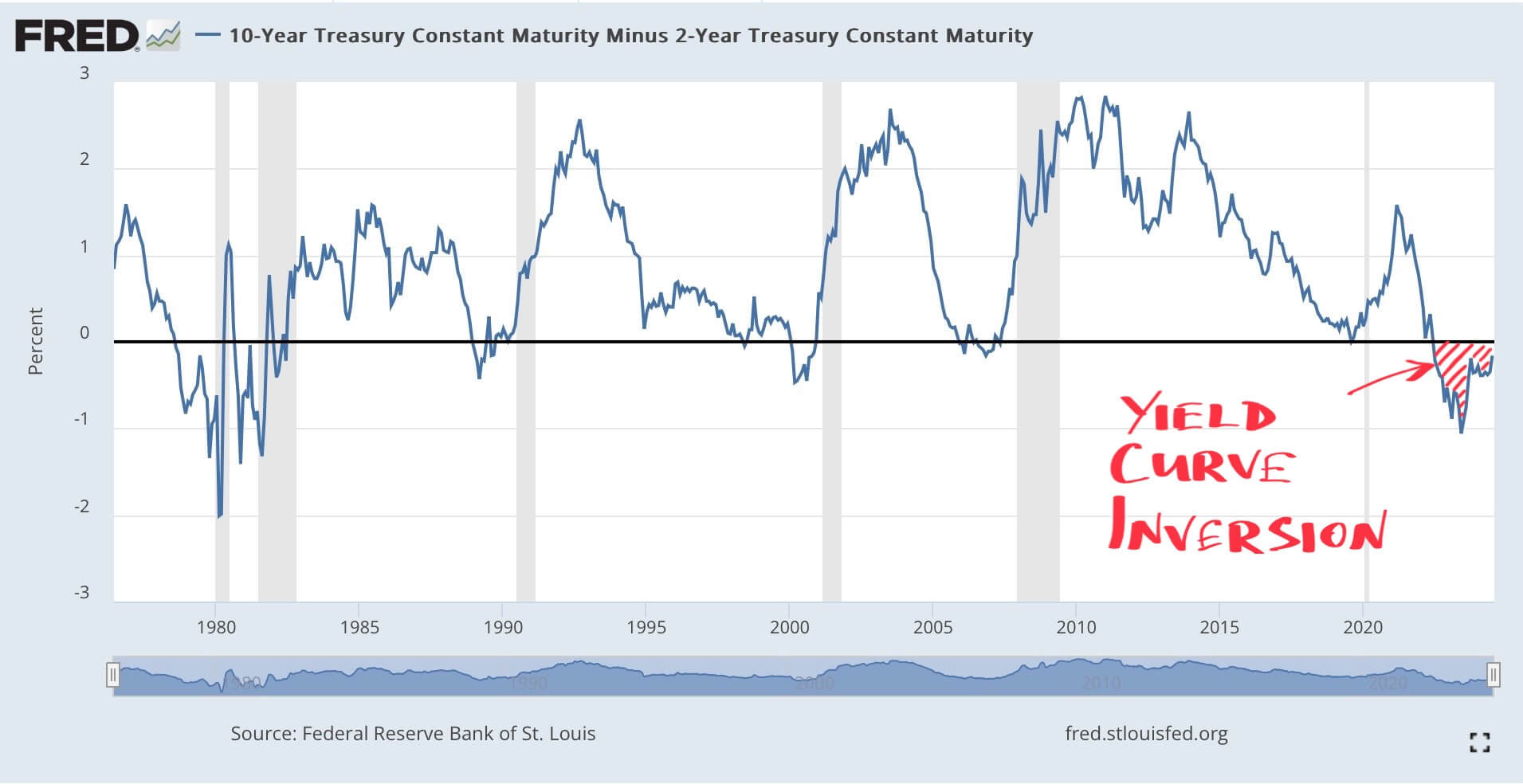

7. US Treasuries

The US Treasuries Yield Curve remains inverted, indicating a possible recession in the future.

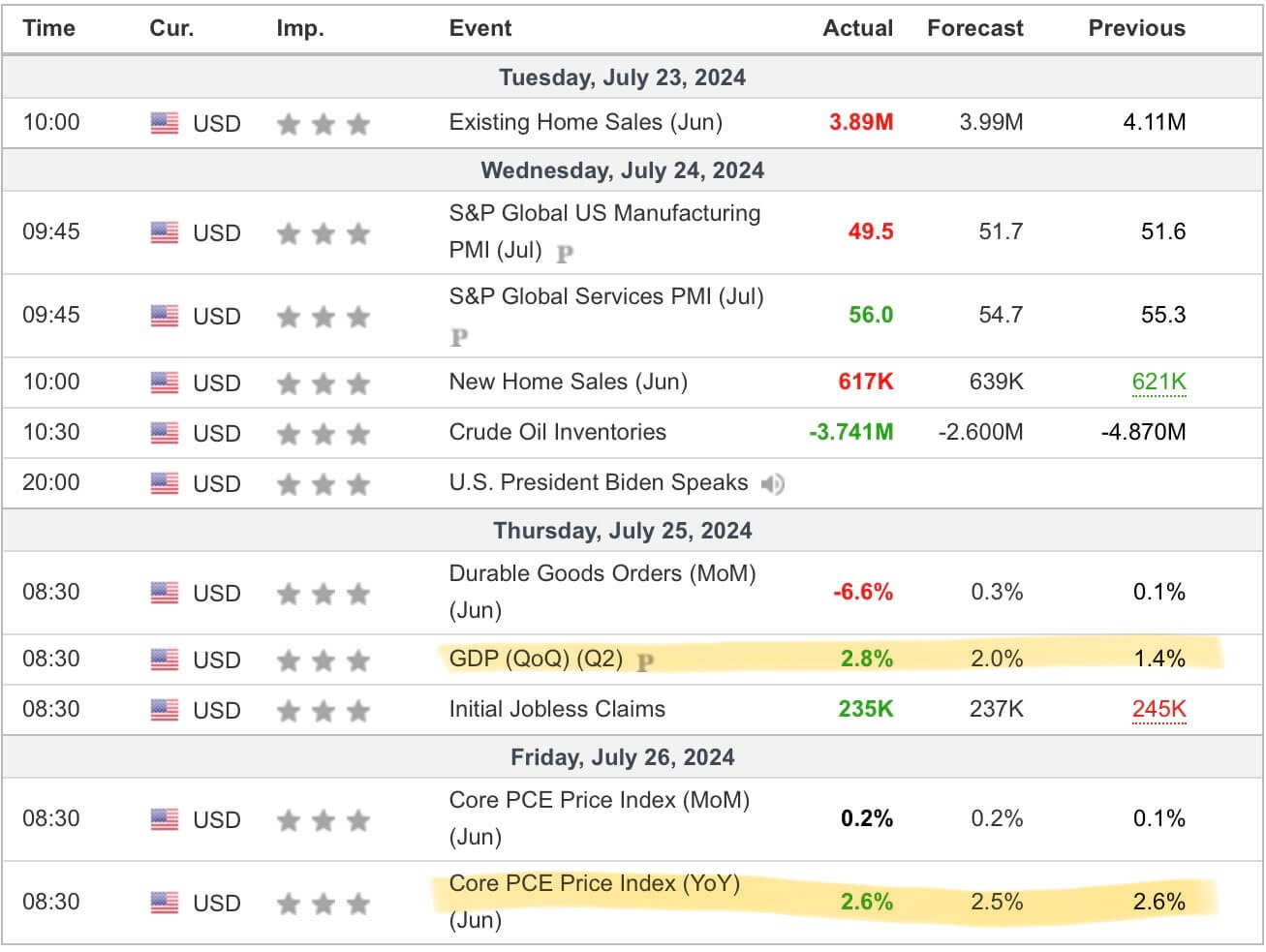

8. Major Economic Announcements

The Federal Reserve's key inflation rate came in slightly hotter than expected in the second quarter, as U.S. GDP growth perked up after a slow start to the year. (read more: IBD)

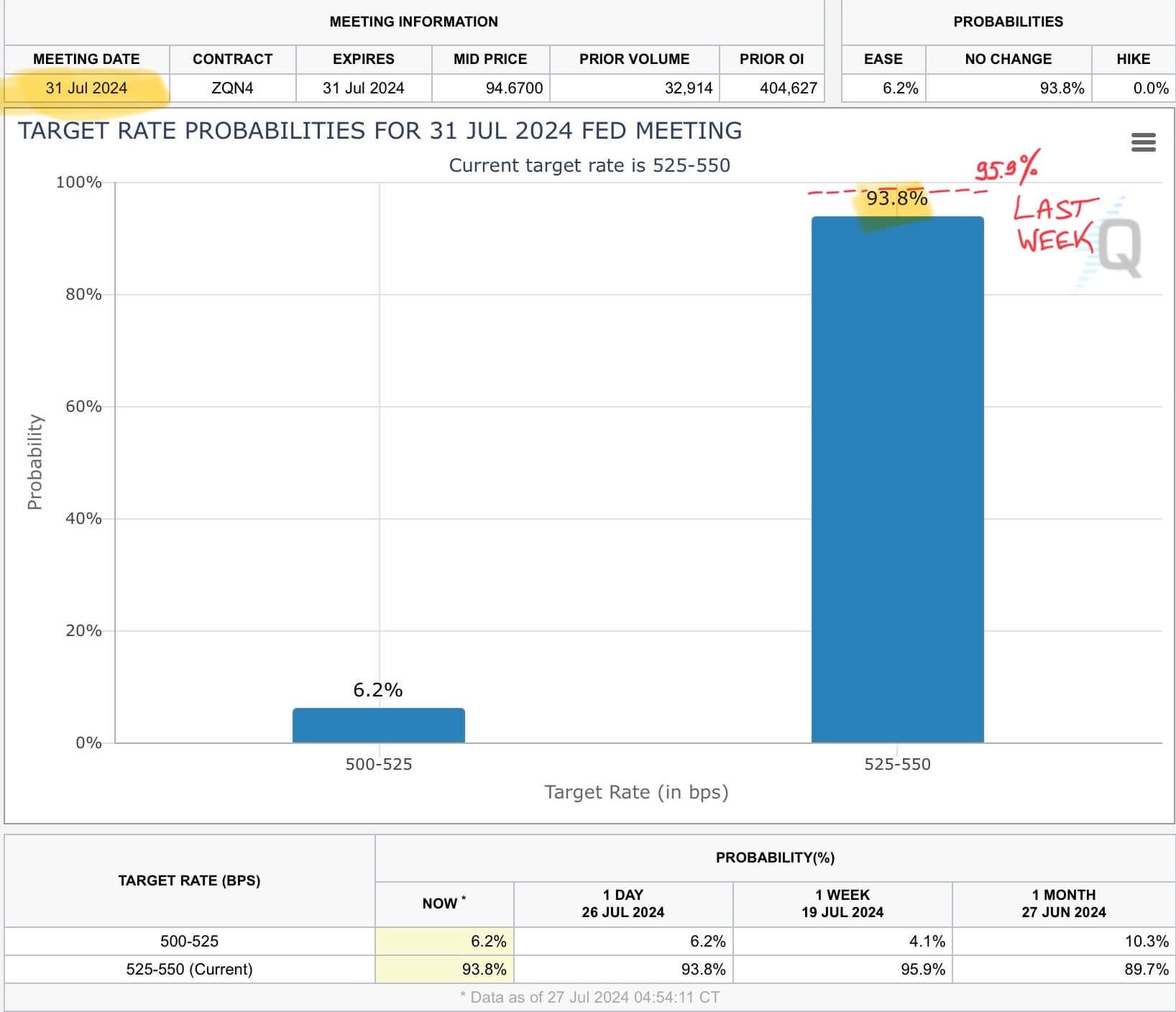

The probability of the FED leaving the interest rate unchanged during the July 31 meeting dropped from 95.9% to 93.8%.

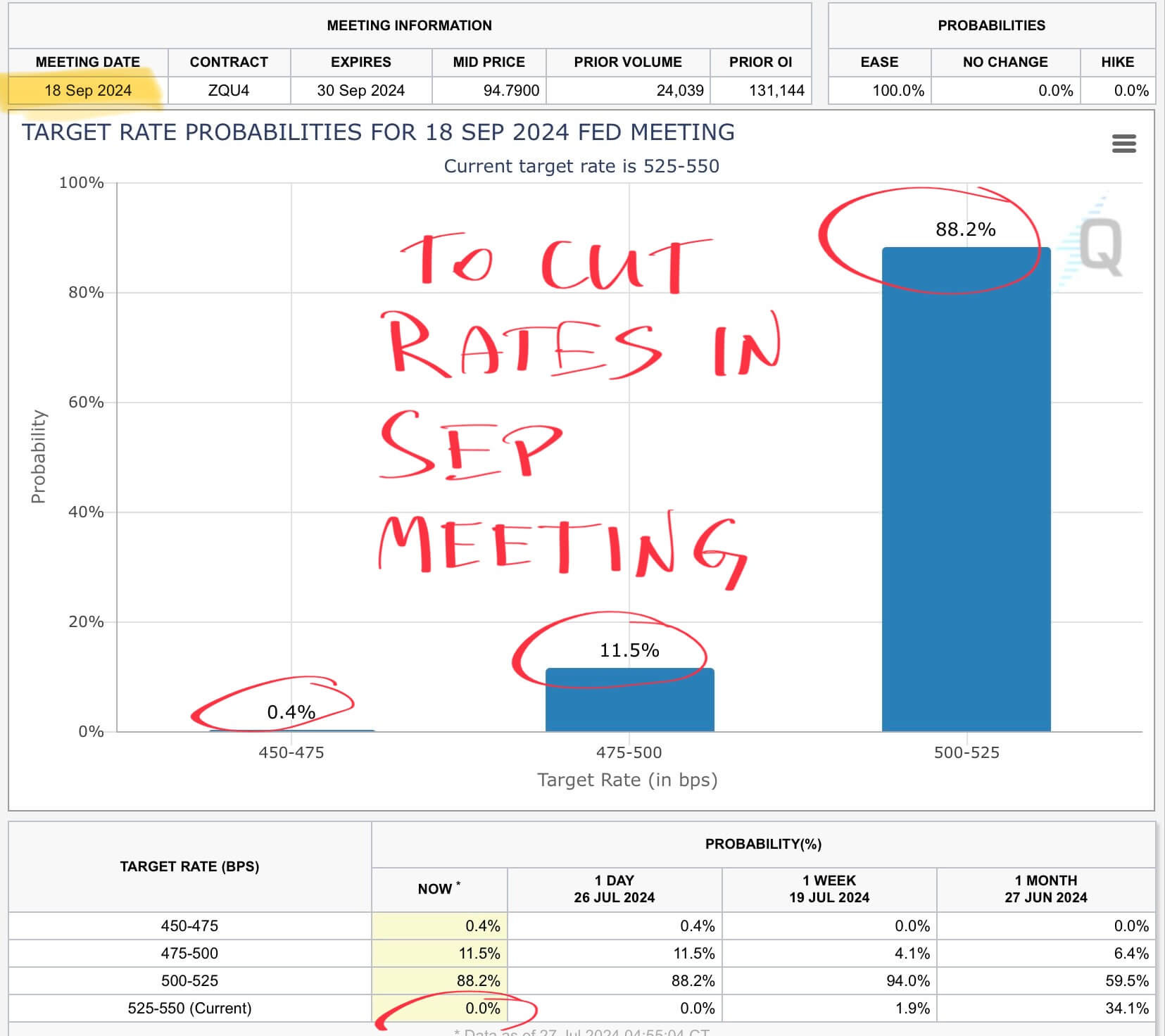

However, there is a 0% probability that the rate will stay the same after the September 2024 meeting.

9. Earnings Reports

Verizon (VZ) was the largest company to report earnings on Monday.

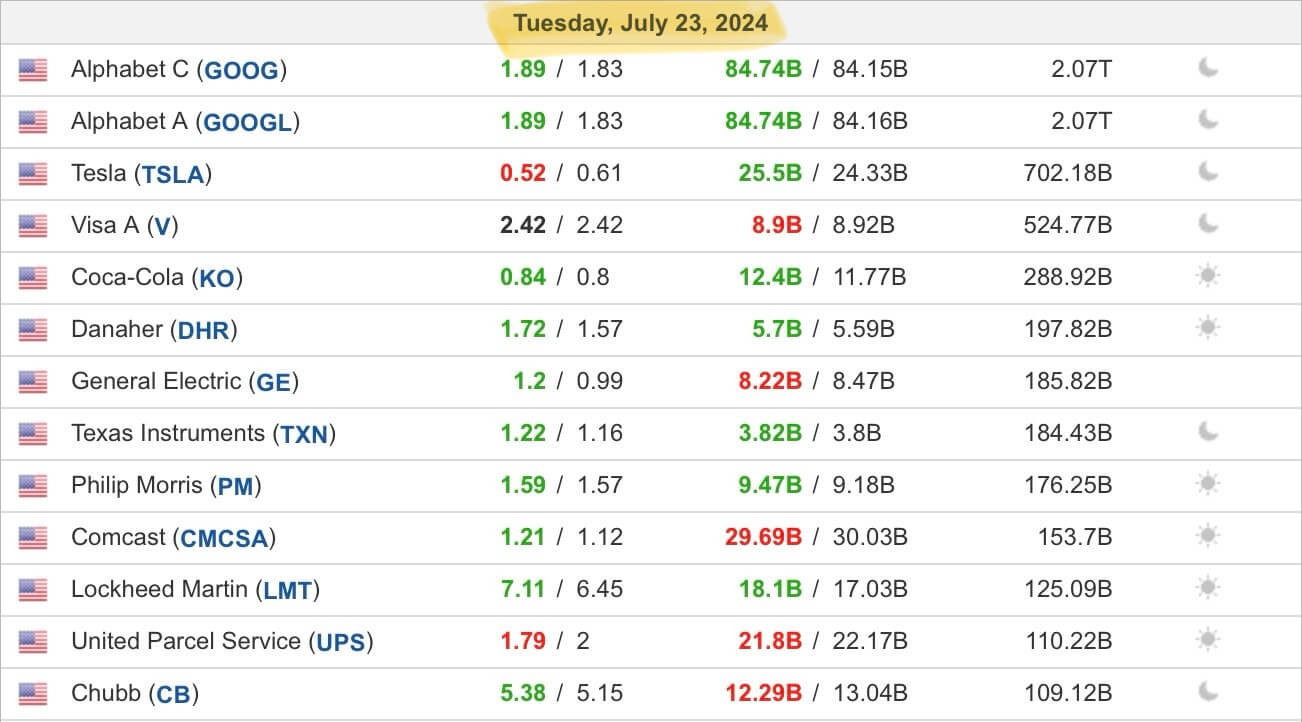

Tueasday was a big day with Alphabet (GOOG), Tesla (TSLA), Visa (V), Coca-Cola (KO) and others reporting their earnings.

Tuesday was a big day with Alphabet (GOOG), Tesla (TSLA), Visa (V), Coca-Cola (KO), and others reporting their earnings.

The Nasdaq plummeted 650 points on its worst day of 2024 as Google and Tesla earnings dragged down stocks. High AI capital expenditures at Google and the disappointing performance of its YouTube division sent Alphabet’s stock down. Tesla investors were especially disappointed by the company’s declining profits due to recent EV discounts and heavy AI spending. (read more: qz.com)

Thermo Fischer Scientific (TMO), IBM (IBM), and ServiceNow Inc (NOW) reported their earnings on Wednesday and exceeded investors’ expectations.

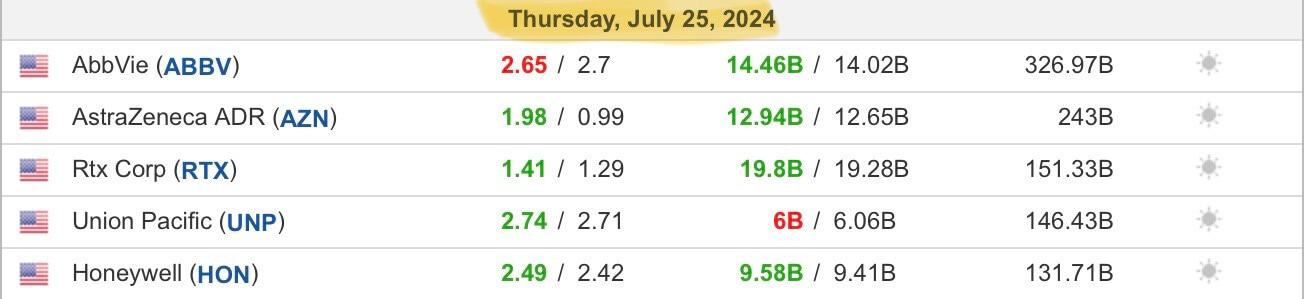

AbbVie (ABBV) and AstraZeneca ADR (AZN) were the largest companies to report their earnings on Thursday.

Bristol-Myers Squibb (BMY), Colgate-Palmolive (CL), and 3M (MMM) reported on Friday and exceeded investors’ expectations.

Next Week

1. Major Economic Announcements

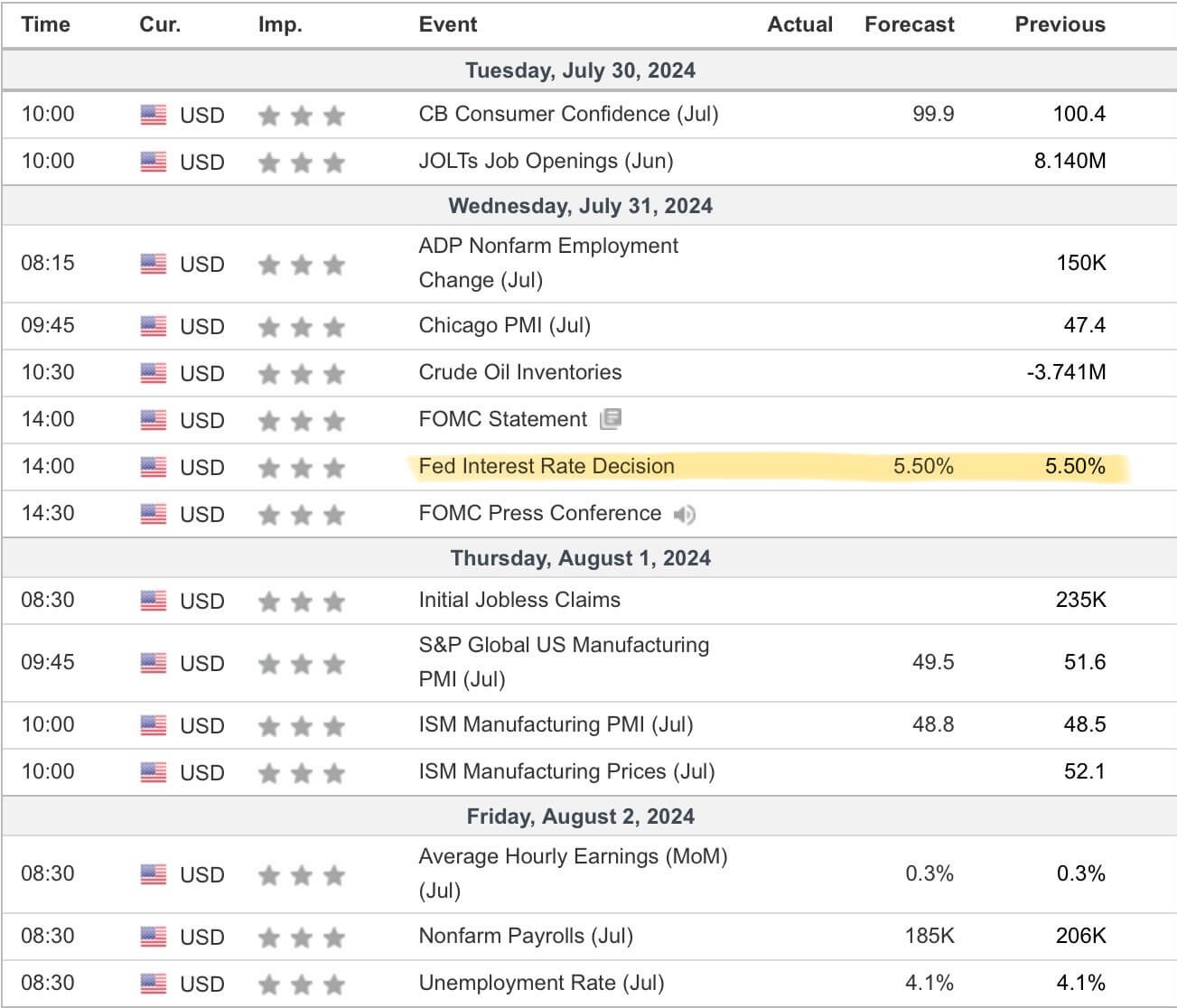

Next week, we will pay attention to the Fed Interest Rate Decision coming out on Wednesday (31 July 2024), although the rate is expected to remain unchanged.

2. Earnings Reports

McDonald’s (MCD) is the largest company to report earnings on Monday.

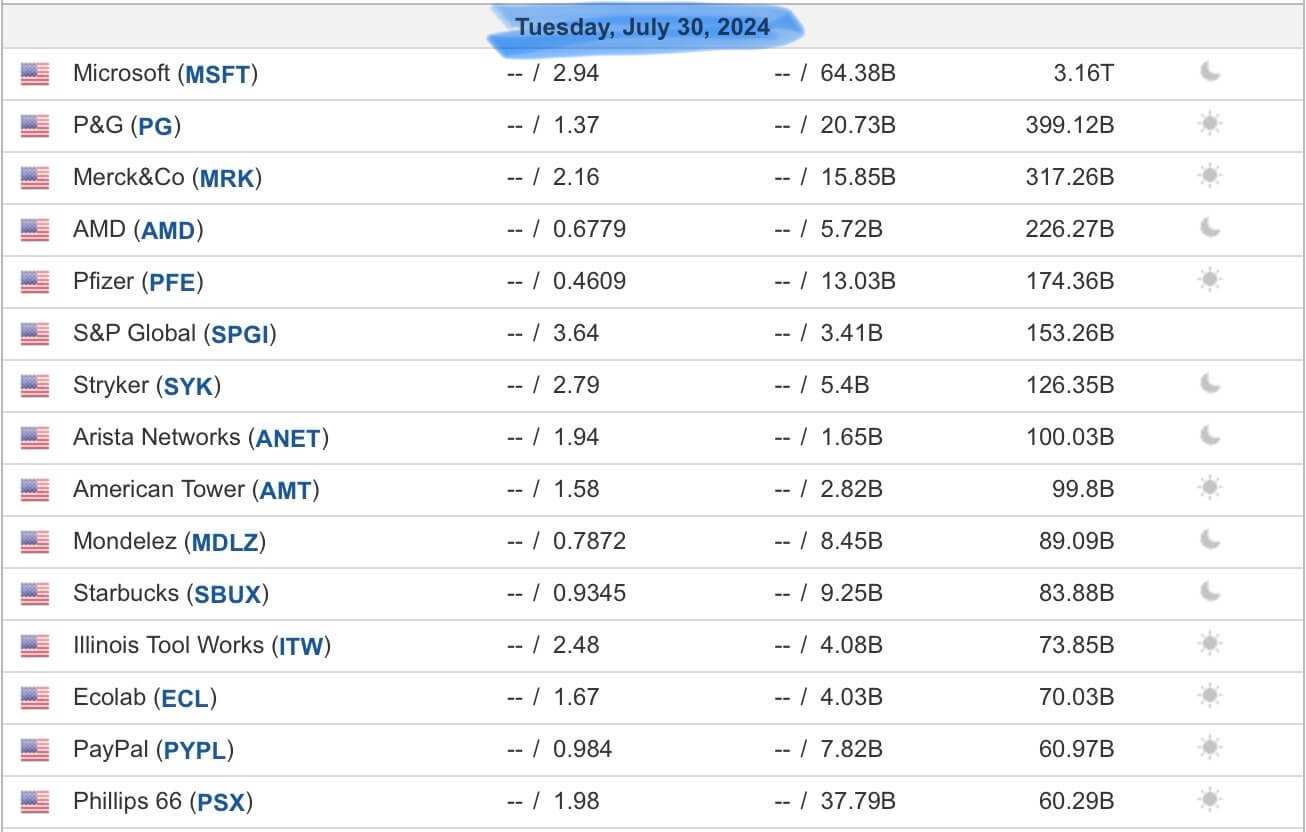

Tuesday will be a big day with Microsoft (MSFT) and other mega cap stocks reporting their earnings.

Meta (META), Mastercard (MA), and Arm (ARM) will report their earnings on Wednesday.

On Thursday, Apple (AAPL) and Amazon.com (AMZN) will report their earnings. This will definitely move the markets on Friday.

Oil giants Exxon Mobil (XOM) and Chevron (CVX) will report on Friday morning.

3. Expected Move

The options market anticipates that the S&P 500 is likely to move +/- 1.8% next week.

Happy trading and investing! 🤑📊🚀

The next email will be sent on Sunday (4 Aug 2024).